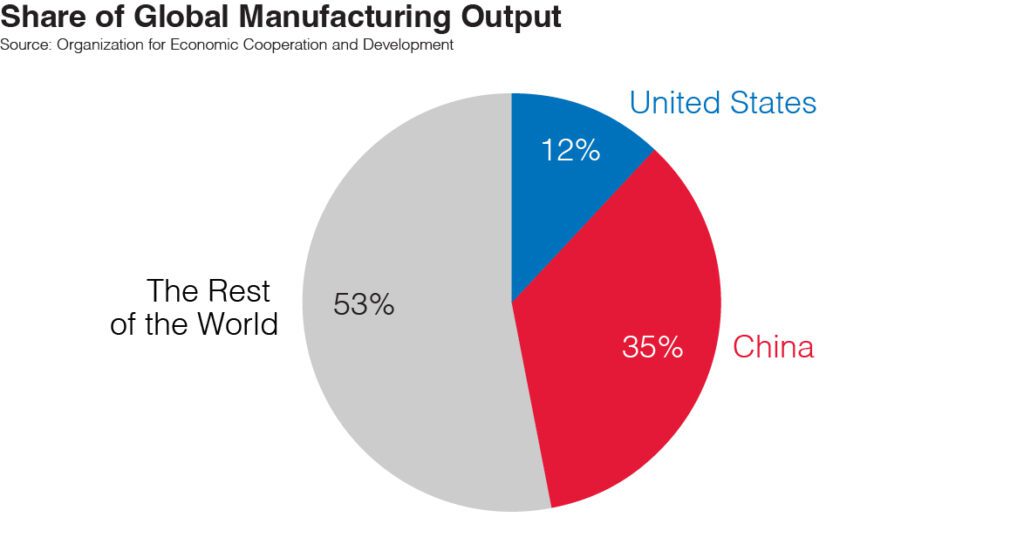

Recent data on global manufacturing output spotlights a stark reality: China now accounts for 35 percent of the world’s manufacturing, nearly three times the United States’ share. The remaining 53 percent is spread across the rest of the world. This concentration is of strategic significance. Manufacturing underpins innovation ecosystems, supply chain resilience, national security, and long-term economic competitiveness.

For the United States, the declining share of global manufacturing is both an economic concern and strategic vulnerability. When production moves abroad, so too do the associated R&D investments, talent pipelines linked to advanced industries, ability to shape global standards, capability to secure and produce critical inputs, and technological leadership. Semiconductors illustrate this vividly: the enormous cost of reshoring production and expanding domestic talent underscores the risks of overreliance on foreign manufacturing.

In an era where supply chains are increasingly intertwined with geopolitics, domestic capability in biotechnology, emerging materials, advanced energy systems, critical minerals, and, yes, semiconductors is essential. The United States cannot afford to rely heavily on external production for technologies that define both economic strength and national security.